I. CHINA’S MACROECONOMIC PERFORMANCE

? China’s economic growth continued to fall. May recorded a manufacturing PMI of 48.8, 0.4 percentage points down from April. Large-sized manufacturers’ PMI was 50.0, 0.7 percentage points up from April; that of medium-sized manufacturers was 47.6, 1.6 percentage points higher than in April; and that of small ones, 47.9, 1.1 percentage points up from April.

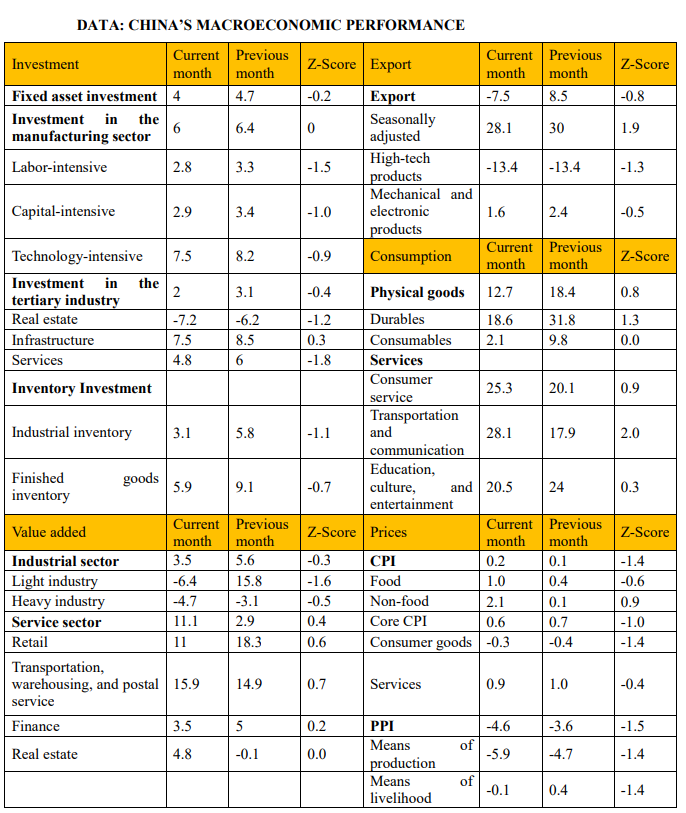

? Industrial production declined. In May, the value added of industries above the designated scale nationwide grew by 3.5% year on year, a decrease of 2.1 percentage points from April. Specifically, value added by manufacturing increased by 4.1% year on year; that of mining by -1.2%; that of power, heat, gas, and water suppliers by 4.8%; that of general and specialized equipment manufacturers by 6.1% and 3.9% respectively; and that of high-tech manufacturers by 1.7%. From January to April of 2023, the total profit of industrial enterprises above the designated scale decreased by 20.6% year on year.

? Export fell sharply. USD-denominated export decreased year on year by 7.5% in May, 16 percentage points down from April; imports dropped year on year by 4.5%, 3.4 percentage points down from April. China pocketed a trade surplus of 65.81 billion USD from April to May, 24.4 billion USD lower than in April.

? Consumption declined. In May, China’s total retail sales of consumer goods picked up year on year by 12.7%, 5.7 percentage points down from April. Specifically, retail sales of goods rose year on year by 10.5%, 5.4 percentage points down from April; revenue of catering services ascended year on year by 35.1%, down by 8.7 percentage points from April. Automobile sales increase year on year by 24.2%, 13.8 percentage points down from April. From January to May, total online retail sales nationwide increased year on year by 13.8%; online sales of physical goods, accounting for 25.6% in total retail sales of consumer goods, climbed year on year by 11.8%.

? Fixed asset investment decreased, with real estate investment continuing to decline. From January to May, nationwide fixed asset investment grew at a cumulative year-on-year rate of 4.0%, 0.7 percentage points down from that in January to April. Private fixed asset investment grew at a cumulative year-on-year rate of -0.1%, 0.5 percentage points down from that in January to April. Specifically, investment in the manufacturing sector increased cumulatively by 6.0% year on year; infrastructure investment in the tertiary sector by 7.5%; and real estate investment by -7.2%, 1.0 percentage points less than that in January to April. From January to May, floor areas sold of commercial housing went down cumulatively by 0.9% year on year, 0.5 percentage less than that in January to April; floor areas of newly started commercial housing fell at a cumulative year-on-year rate of 22.6%, 1.4 percentage points less than that in January to April.

? CPI remained low, and PPI continued to fall. May CPI grew 0.2% year on year, up 0.1 percentage points from April. Non-food prices grew 0% year on year, down 0.1 percentage points from April; food prices grew 1.0% year on year, down 0.6 percentage points from the previous month. The core CPI excluding food and energy grew 0.6% year on year, down 0.1 percentage points from April, while the PPI grew -4.6% year on year in May, recording a 1.0 percentage-point bigger drop than the decrease in April. Specifically, the factory prices for production materials grew -5.9% year on year, and living materials grew -0.1% year on year, down 1.2 and 0.5 percentage points from April.

II. MACROECONOMIC ENVIRONMENT

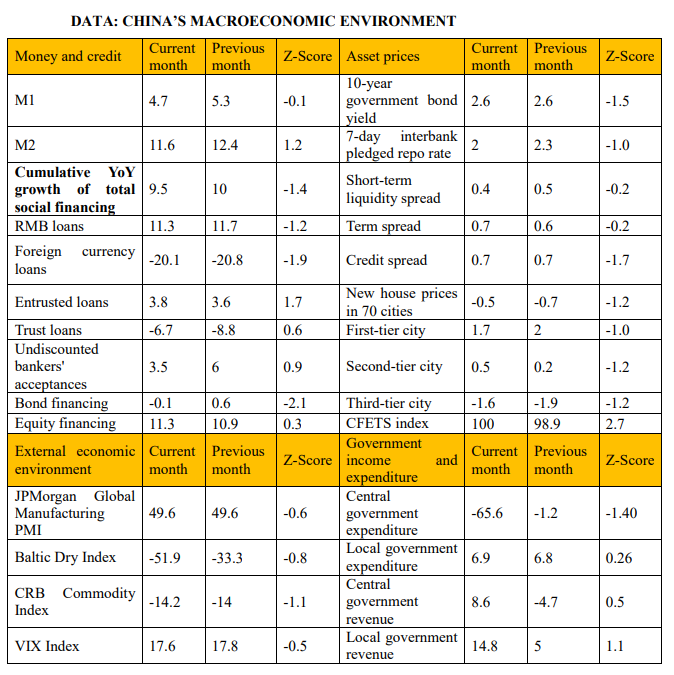

? The global economy rebounded. The J.P. Morgan Global Composite PMI rose to 54.4 in May, up 0.2 percentage points from April; the J.P. Morgan Global Manufacturing PMI was 49.6, the same as the previous month. Manufacturing PMI in the United States declined to 46.9 in May from 47.1 in April, while that in the Eurozone fell to 44.8 in May from 45.8 in April, and that in Japan rebounded from 49.5 in April to 50.6 in May. CRB spot commodity prices fell 0.9% month on month.

? The growth of social financing declined. The year-on-year growth rate of M1 in May was 4.7%, down 0.6 percentage points from April; that of M2 was 11.6%, down 0.8 percentage points from April. Social financing growth was 9.5% year on year, down 0.5 percentage points from April. May recorded newly added social financing of 1.6 trillion yuan, an increase of 0.3 trillion yuan from April. Among them, newly issued government bonds (government bonds + local government bonds + special bonds) totaled 600 billion yuan, up 100 billion yuan from April; newly issued corporate bonds stood at 0.6 trillion yuan (LGFVs included), down 0.4 trillion yuan from April; new debt of the household sector was 400 billion yuan, up 600 billion yuan from April.

? The 7-day repo rate fell. The 7-day interbank pledged repo rate averaged 1.99% in May, down 30 basis points from April. The short-term liquidity spread represented by the difference between the 3-month SHIBOR and the 3-month government bond yield was 0.45%, down 2 basis points from April. The term spread, represented by the difference between the 10-year government bond yield and the one-year government bond yield, increased by 4 basis points from April to 0.66%; the credit spread, represented by the difference between the 10-year AAA-rated bond yield and the 10-year government bond yield fell by 1 basis points from April to 0.66%.

III. NEAR-TERM OUTLOOK AND RISK WARNING

1. Lack of domestic demand continues to be a major obstacle to the current economic recovery.

2. Excessive real interest rates are dragging down the expansion of social credit, leading to a lack of spontaneous market demand.

3. Downward external pressures are weighing on exports.

IV. POLICY SUGGESTIONS

1. Lower the interest rate by 25 bps each time until the employment and growth targets are hit.

2. Issue new types of fiscally subsidized bonds and policy loans to support investment in public and quasi-public infrastructure projects that feature limited returns.

3. Set up special funds to help market entities battered during the pandemic get back on their feet; increase the amount of living allowance for low-income groups.

4. Stabilize normal financing for real estate companies; introduce market-based competition on mortgage rates to reduce households’ debt burdens. To resolve the developers’ debt burdens, conduct pilot projects to convert some of the developers’ housing stock into government-subsidized housing.