Abstract: In this article, the author discusses transformation of China’s infrastructure investment from four aspects, i.e. structural change of infrastructure investment over the past decade, role of infrastructure in expanding social credit and maintaining economic growth, current problems with infrastructure development, and how to improve the financing and planning of infrastructure projects.

I. CHANGES IN THE STRUCTURE OF CHINA’S INFRASTRUCTURE INVESTMENT

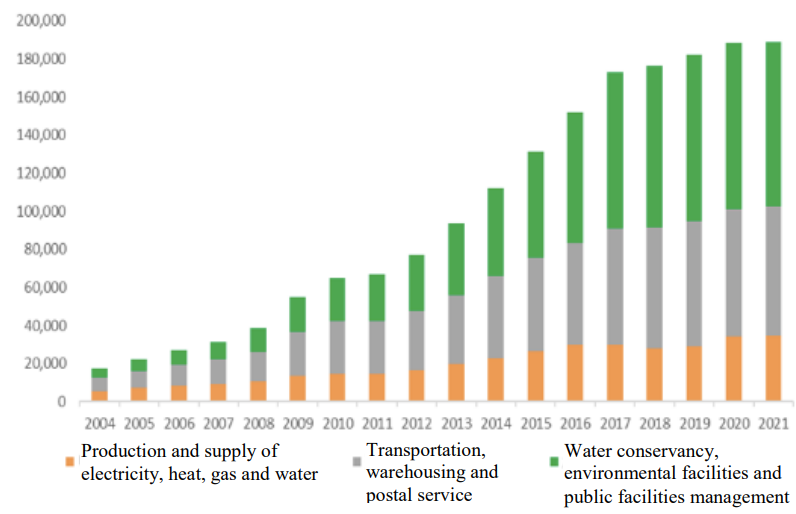

According to the data from the National Bureau of Statistics, the scale of China’s infrastructure investment was between 17-18 trillion yuan in the past few years. The statistics take into account three categories: The first is transportation, warehousing and postal services, with railway, road and aircraft transportation included, recording a scale of about 6-7 trillion yuan; the second is the production and supply of electricity, gas and water, with a scale of about 2-3 trillion yuan; the third is water conservancy, environmental facilities and public facilities management, standing at 8-9 trillion yuan. Now there is a concept of new infrastructure, involving seven areas. In fact, most of the seven areas of new infrastructure can be included in the statistics of traditional infrastructure investment, but some may not. In the past, about 14-15 trillion yuan of the 17-18 trillion yuan infrastructure investment was undertaken by the government and government-controlled companies, and 2-3 trillion yuan came from private capital.

According to statistics by the National Bureau of Statistics, the structure of infrastructure investment has undergone significant changes over the past decade. Most notably, the proportion of investment in electricity and gas industries has declined, and the growth is rather limited; also falling is the proportion of investment in transportation and warehousing. The proportion of investment in urban public facilities management rose rapidly, but the growth has slowed since the outbreak of the pandemic. Over the past ten years, the proportion of investment in water conservancy, environmental facilities and public facilities management has witnessed rapid growth. These are changes in the structure of infrastructure investment.

Figure 1: Changes in the structure of China’s infrastructure investment (2004-2021)

In terms of overall size, 2018 was a turning point. Infrastructure investment had maintained a growth rate of 15-20% until 2018. The growth dropped dramatically since 2018, and the fall was especially severe in the past two years of the pandemic, recording no growth at all.

Reasons behind the change can be discussed from multiple aspects. On the one hand, structural changes in infrastructure investment can be a result of changes in industrial and demand structure. A lot of infrastructure investment by state companies such as that in electricity and transportation was made during the process of rapid industrialization. Nowadays, as industrialization and manufacturing growth slows, and the importance of the service sector grows, the demand for infrastructure construction has tilted toward urban public facilities, water conservancy, and environmental facilities. On the other hand, in recent years, especially in the first two years of the pandemic, the construction of urban public facilities slowed down significantly, which was caused by efforts to tackle local government debt, the narrowing of financing channels, reduced enthusiasm of local governments to invest in infrastructure as well as the pandemic.

II. THE ROLE OF INFRASTRUCTURE

The role of infrastructure is a research focus in academia, especially the study on China's high-speed rail and highway. This type of research does not evaluate the benefits of a project itself, but the reduction of transportation costs for personnel and logistics because of the project, and the positive spillover effects on the local economy, including on exports, population movements, and industrial structure changes and agglomeration economies, etc. Plenty of studies in this field have been done in China. Overall, the general conclusion is that transportation infrastructure has had a positive effect on economic growth.

At present, investment in urban public facilities records higher growth compared to other types of infrastructure. But there is very little research on this part in academia, probably because relevant data is not easy to obtain, and related theories are not complete. These projects are more of public goods and quasi-public goods in nature, and the evaluation focuses more on their spillover effects, including scale effects, so it’s not easy to assess the impact. In any case, it can be seen from daily life that these water conservancy, environmental and urban road facilities (mainly urban roads, bridges, drainage system, flood control system, lighting facilities and underground pipes) are essential parts of urban life.

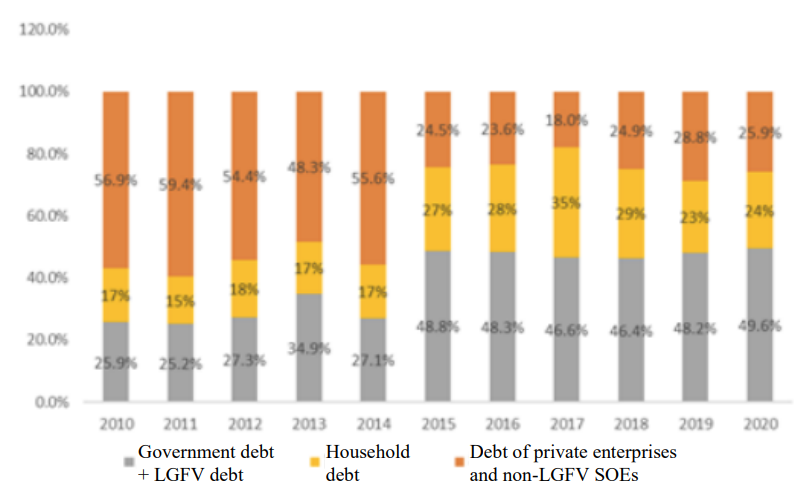

In addition to their benefits and spillovers, infrastructure projects have played an unheralded role in supporting credit creation and stabilizing the macro-economy in the last decade. Infrastructure investment has aided not only credit growth and economic performance of the country but also economic and social stability locally. In recent years, the increase in the debt of government and local government financing vehicles (LGFVs) has accounted for about half of all debt increases, compared to 1/4 a decade before. It is sufficient to state that behind the growth in social credit, there has been a significant increase in LGFV debt, which is primarily used for infrastructure.

Figure 2: Government debt, corporate debt, and household debt in overall debt increases (2010-2020)

However, many argue use of new debt for infrastructure investment has brought about dangers and concerns, including crowding out of investment by the private sector. Data show that an increase in infrastructure investment is frequently accompanied by an increase in private investment in fixed assets. In addition, growth of infrastructure investment at constant prices has not led to a rise in the interest rate.

Then, we could take a look at other countries at a similar stage of development during the post-industrial peak period. When productivity improvements and corporate ROI peaked, most countries experienced a drop in demand for credit, which could then slow the growth of purchasing power, resulting in insufficient demand and economic slowdown. When we look at Germany, France, and Japan in the 1970s and 1980s, as well as South Korea after the 1990s, we can see a general trend: after the economy transitioned from being manufacturing-driven to being services-led, corporate debt growth slowed dramatically. At similar phases in the four countries, the growth of corporate debt/GDP was relatively tiny, household debt growth was slightly higher, and the government sector was the most essential aspect of sustaining credit and debt growth. The government debt/GDP ratio in Japan surged by 5.6 times between 1970 and 1990; the debts were mostly employed for two purposes: infrastructure and social security spending.

Turn back to China. China’s government debt/GDP ratio rose by 3 times from 2012 to 2021 in the most broad-based standard for debt, which includes the government bond, special bond, and implicit debt of LGFVs. Credit demand and debt expansion, particularly corporate debt expansion, have slowed, as they have in other nations, but the government has made up the gap. China does not stand out in terms of the growth of government debt/ GDP ratio, even when the broadest measure of implicit government debt is used. In actuality, credit expansion made possible by infrastructure investment is a vital support for maintaining cash flows in many regions. Therefore, infrastructure plays a key role in maintaining macroeconomic stability, supporting credit growth, and boosting demand.

III. PROBLEMS WITH INFRASTRUCTURE INVESTMENT

Problems with infrastructure projects are examined from two perspectives: financing and investment.

Infrastructure financing is closely related to high leverage and financial irregularities that have yet to be resolved. As previously said, the focus of China’s infrastructure construction has shifted significantly from lucrative railway, highway, and airport projects to less profitable urban public utilities such as underground pipe networks, urban roadways, bridges, lighting, greening, and scenic locations.

On the one hand, infrastructure projects are becoming less and less profitable, but society needs them. On the other hand, these projects use high-interest and short-term funds from commercial financial institutions instead of the cheapest funds from public finance, and later also use shadow banking loans with interest rates as high as 10-15%. With such a rapid increase in borrowing and high interest rates, it is only natural for the debt to skyrocket.

Another significant issue in infrastructure financing is that many local governments face ‘soft budget constraints’, and they do not intend to pay back debt on some projects, which has led to excessive government borrowing.

The two aspects – costly funds for unprofitable projects and a soft budget constraint – are the sources of financial irregularities, rising leverage, and systemic financial risks. It's not a justification to abandon infrastructure or dismiss the necessity for economic stimulus in the face of a downturn; it simply indicates that the funding approach is flawed - that commercial financial institutions are financing government projects.

The central government's budget for infrastructure construction is currently over 1 trillion yuan, and half of the government’s 14 or 15 trillion infrastructure projects are not profitable. The government has reduced some debt burdens in recent years through debt replacement, issuance of special debts, and better management of local government implicit debts, but the problems have not been fixed. There is still a structural mismatch between supply of and demand for infrastructure funding.

From the perspective of infrastructure investment, unreasonable regional layout is a major issue. Infrastructure is, after all, for people. Infrastructure should follow where people and industries go. However, this is not the case in reality. Infrastructure thrives in towns with large population and industry outflows. Such infrastructure is designed to maintain the operations of local governments, enterprises, and certain groups, resulting in a huge amount of bad debt and loss of efficiency.

Based on relevant indicators including population inflow, industrial development, economic performance, and the solvency of LGFVs, we split infrastructure into two categories - safe and unsafe. Infrastructure projects in major cities are safer judging from their investment efficiency and solvency. Constructing infrastructure in third-tier or smaller cities is less beneficial in terms of contribution to GDP growth and project solvency.

There are also issues with project design, and facilities have problems, too. For example, the fifth and sixth rings of Beijing have been equipped with roads, lights, and buildings, but why are these areas in such disorder? It is because there is a lack of supporting facilities like parking lots and traffic management personnel.

IV. SUGGESTIONS

1. The Role of Infrastructure

To put it another way, infrastructure investment is a form of government debt expansion, which is a crucial policy tool for maintaining credit growth and expanding domestic demand. In the current economic slump, infrastructure investment is required, not only to bring in more projects but also to expand social credit and boost the overall income level of society. In a time of low demand, increased infrastructure investment could have positive spillovers on other sectors, and it is also beneficial to private investment, as it improves the cash flow and prosperity of private businesses.

2. Infrastructure Financing Channels

In the past, unproductive infrastructure projects could be carried out because they were financed with local revenue from land sales, but that revenue is now rapidly dwindling. Many real estate analysts believe that China's housing sales have peaked, and that future sales will be unlikely to approach 1.6 or 1.7 billion square meters, which will drag down the revenue from land sales. This will result in a significant infrastructure financing deficit, forcing the government to seek out good funding channels. Overall, financing for infrastructure can be obtained from the following sources:

(1) Use low-interest and long-term funds such as government bonds or general debt financing for public interest or quasi-public interest projects;

(2) Prefer loans from policy finance institutions such as China Development Bank to commercial ones.

(3) Provide government subsidies for REITs. REITs require returns. Many infrastructure projects cannot guarantee returns, hence the projects are limited in scope. The government could provide interest subsidies which could help increase leverage and attract social capital.

(4) Expand the use of special bonds to supplement infrastructure financing from multiple sources.

Either way, the basic principle is that the government should pay for what it does for public welfare or quasi-public welfare. If it is financed by commercial financial institutions, there will be too many consequences and too much risk.

3. Investment in Infrastructure

Infrastructure should follow the flow of people and industries, and metropolitan regions have great potential for infrastructure construction. Infrastructure investments should be considered not only in terms of commercial returns but also from broader perspectives such as their spillovers and social returns. There is a lot that can be done.

From the perspective of population aging, now in China, 70-80 working-age people are supporting 20-30 seniors, but in two or three decades, the ratio will be 50 - 50. The real challenge is not how much money we have in the pension fund. If pension income increases, other social benefits should be cut, otherwise there will be inflation and the money in the pension account will be worth less. The real challenge lies in the transition from 70 supporting 30 to 50 supporting 50. We should get more work done now to reduce the burdens of future working-age population so they could focus on supporting the senior group. So, from a demographic point of view, we also need some ahead-of-schedule infrastructure developments.

This article is the transcript of a speech made by the author at the monthly seminar of Bozhi Macroeconomic Forum held by China Development Research Foundation. It is translated by CF40 and has not been reviewed by the author. The views expressed herewith are the author’s own and do not represent those of CF40 or other organizations.