Abstract: Many signs show that economic recovery is on the way in China, although domestic demand is still low. The recovery will neither be explosive nor easy, but will be unbalanced. Lack of demand is the most prominent contradiction facing economic rehabilitation.

I. Developed economies are experiencing what China did two months ago

No variable can now affect our lives and work more than the novel coronavirus pandemic and lead our assessment of the economic situation. We have also come to be fully aware of the complexity and cunningness of the virus as well as the possibility of its co-existence with human beings.

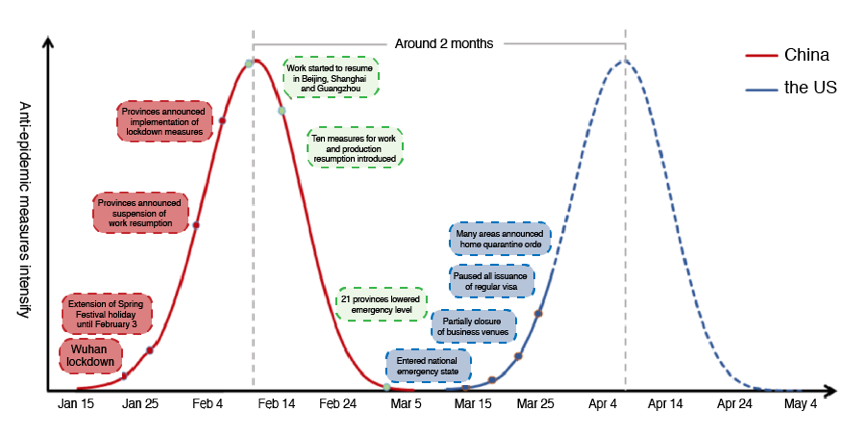

Many developed countries appear to be experiencing what China did two months ago, which is not only reflected in the evolvement of their outbreaks, but also in the shift toward increasingly stringent anti-epidemic measures. Needless to say, each country has different systems, and there is no need to judge whether their practices are good or bad, but the evolution of the epidemics shows that each country has experienced an epidemiological curve which peaked gradually before it began to fall.

Figure 1: Many developed countries are going through what China did two months ago

Source: WIND; compiled by author

Judging from the reaction of the capital market, it seems that investors are not so afraid of the virus. What truly worries us is people's dismissive attitude toward the pandemic or the laws of nature, and their lack of humbleness in the face of the virus.

For China, there are also several concerns: first, whether the epidemic would recur in fall and winter; second, the number of imported cases; third, asymptomatic infected cases.

Not medical experts or virologists, we can only make judgment based on the conclusion drawn in current literature: the novel coronavirus may coexist with human beings for a long time before a vaccine is available, and the possibility of collective immunity should not be ruled out. According to most medical analysis of the evolution of virus, various local outbreaks will likely occur in the future. But in general, even if there is a recurrence, it's unlikely to spike beyond the peaks we've already experienced.

However, the peak has not come yet in many countries, including India and many African countries. Robert Redfield, Director of the Centers for Disease Control and Prevention in the US, also warned in April that the second wave of Covid-19 could hit the US this winter, possibly overlapping with the start of the flu season, thus making the situation more severe.

From the perspective of economic analysis, what we can do at present are: first, find future direction from historical comparisons; second, incorporate new information and modify the judgment based on history.

Throughout human history, there were only a few epidemic outbreaks in the past 100 years, among which SARS was less severe and the Spanish flu is more comparable to the Covid-19 pandemic. But one problem is that the Spanish flu broke out around 1918 when the situation was completely different from today's in many aspects including the extent of globalization and the macro policies.

In 1918, there were neither Keynesianism, nor fiscal and monetary policy instruments. What's more, communication methods were quite different. Therefore, we didn't use the Spanish flu as a very important benchmark, either.

There is no doubt that the epidemic is different from the Wenchuan earthquake or flood disasters. The epidemic has a profound impact on people's physiological and psychological life, as well as the supply and demand in the economy.

In the epidemic, many policies in the early stage were supply-oriented, focusing on relief, promoting work and production resumption, and restoring the labor market, because labor is the most important factor of production in the production function. It is also the case with recent policies in the US, which may appear as fiscal stimulus, but are in fact more about disaster relief as the money is directly given to households, individuals as well as enterprises.

II. Economic recovery is on the way in China

Many signs are showing that although China's domestic demand is still low after the peak of the epidemic, spontaneous recovery is on the way.

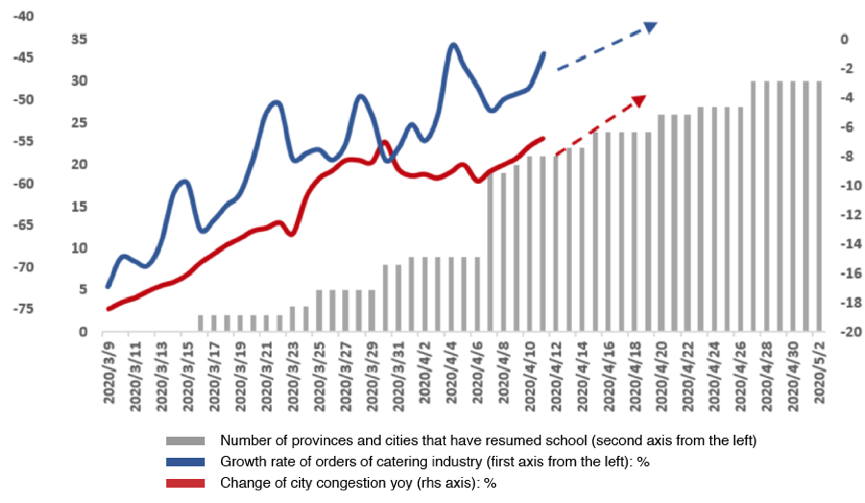

First, services industry such as catering which has been greatly affected by the epidemic, is still struggling. Catering orders are only about half of what they were at the beginning of this year, but have seen some marginal recovery recently.

Figure 2: Services industry such as catering is on the way of spontaneous recovery

Source: WIND

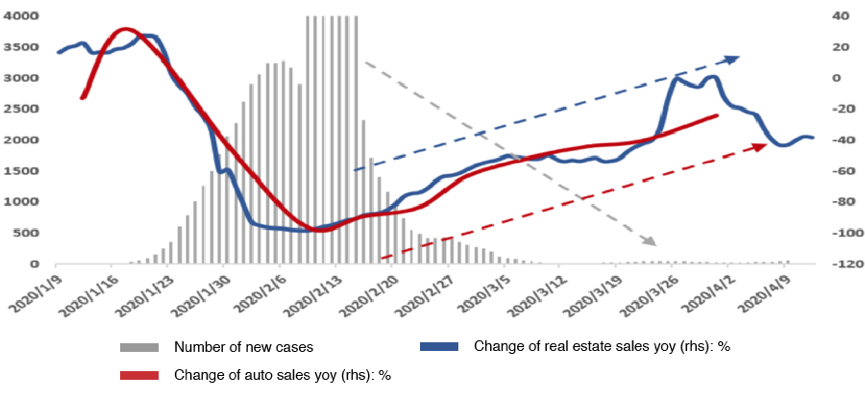

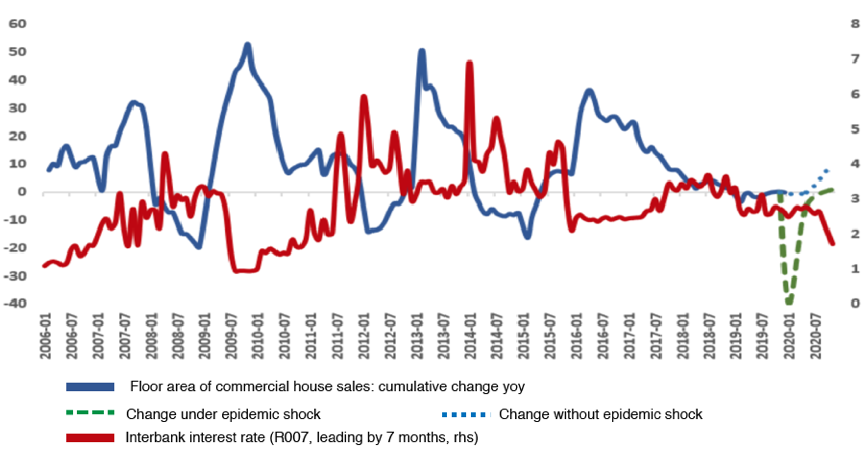

Second, auto and real estate industries began to recover spontaneously. Growth rate of auto sales are mostly back in positive territory, while that of real estate sales are still in negative territory but has been picking up from a steep drop in the first quarter. We haven't seen a strong stimulus for auto and real estate industries, thus the recovery is spontaneous, though limited.

We are more optimistic about the real estate industry. Although China did not cut interest rate by 150 basis points at once as the Federal Reserve did in response to the epidemic, the interbank lending rate in China has been falling continuously, which has positive impact on and is a leading indicator of the real estate sector, according to historical pattern.

Figure 3: Auto and real estate industries began to restore spontaneously

Source: WIND

There are now two driving forces in the real estate market: one is spontaneous restoration; the other is the intensity of counter-cyclical policies. The consumption or sale of real estates is not like that of the tourism or catering industry. Demand for housing will not disappear, but only delayed. With the guidance of interest rate policy, real estate sales are now rising after bottoming out. The whole second quarter will still see negative growth but is heading toward zero growth.

Figure 4: Real estate sales are now rising after bottoming out

Source: WIND

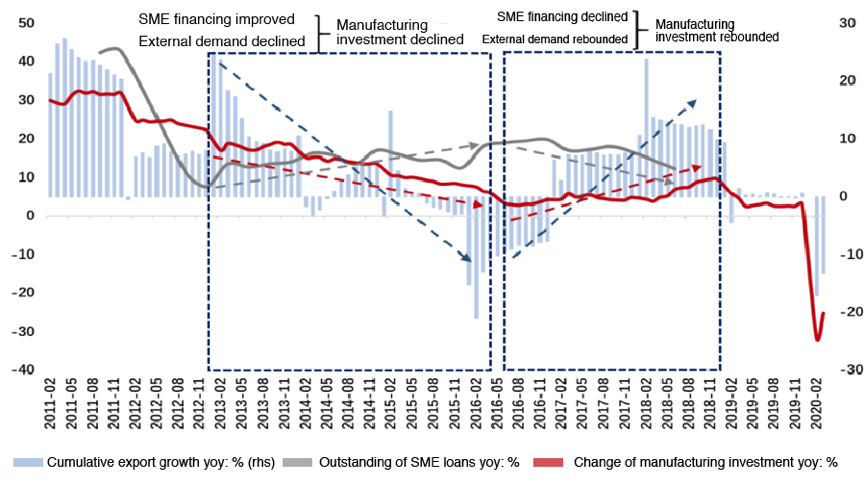

Third, the manufacturing sector will remain under significant pressure because of its high reliance on external demand.

Figure 5: Manufacturing will remain under significant pressure

Source: WIND

III. Lack of aggregate demand is the most prominent contradiction facing economic rehabilitation in China

China is the first country to enter and get out of the Covid-19 outbreak. Although still confronted with imported cases and asymptomatic infections, China has largely brought the virus under control domestically and is the first country to resume work, production and school.

After the epidemic is controlled, China needs to prevent the recurrence of the virus, and more importantly, to restore the economy.

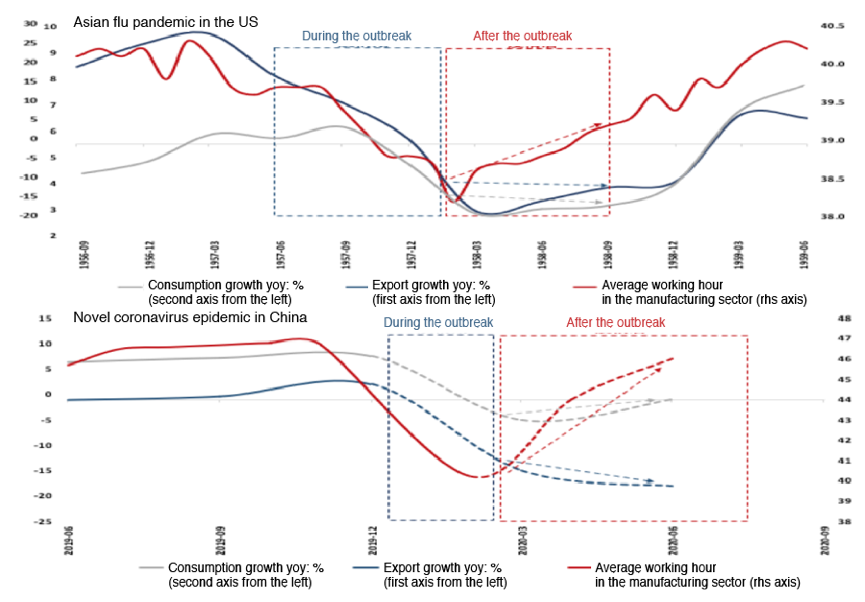

What is the main contradiction in post-disaster reconstruction? The supply side of the US economy restored quite fast after the 1957 Asian flu pandemic. This is quite similar to the current situation of China, that is, relative to the demand side, the speed of work and production resumption is very fast, indicating that the restoration of supply is fast.

Figure 6: Comparison of economic restoration in China and the US after the Covid-19 epidemic and the 1957 Asian flu pandemic

Source: WIND; author's calculation

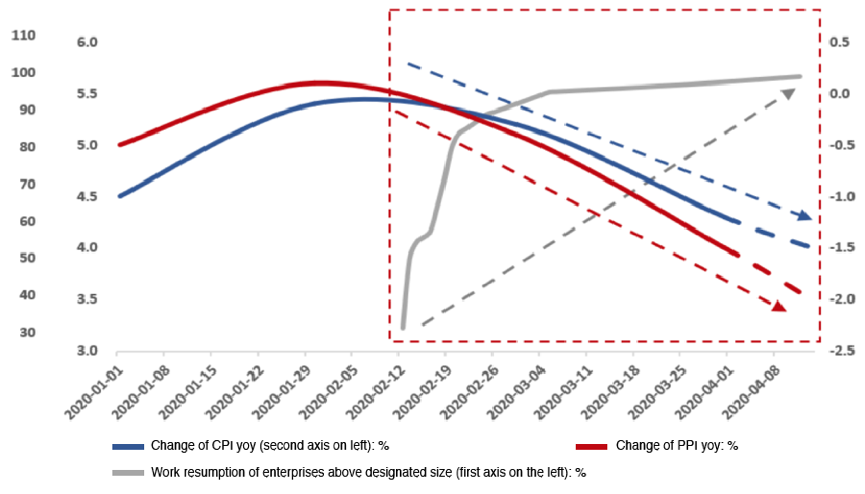

Of course, supply is not fully restored right now, but in a relative sense, supply is sufficient while demand is insufficient.

There are two indicators that could be used to measure whether supply or demand is the main contradiction in the economy, that is, inventory and price. If inventories are now passively accumulated while PPI and CPI are trending down, it indicates that the main contradiction in the economy is insufficient aggregate demand, rather than insufficient supply. This judgement is key for macro policy making.

Figure 7: Insufficient aggregate demand relative to supply is the main contradiction

Source: WIND; local government portals; author's calculation

Although there is a lack of demand, it can be seen from the high-frequency data that many services industries including catering are actually seeing marginal restoration, which is a spontaneous process rather than the outcome of policy stimulus. Because so many people are returning to work and ordering take-outs, the food services industry is recovering spontaneously. The congestion index is also going up.

However, such restoration is neither explosive nor easy. For instance, if the consumption of haircut service was zero in February and delayed to March, of course the number would jump in March. But what about in April or May when things are back to normal? Such brief jump in consumption is limited, which is linked to the internal mechanism of consumption.

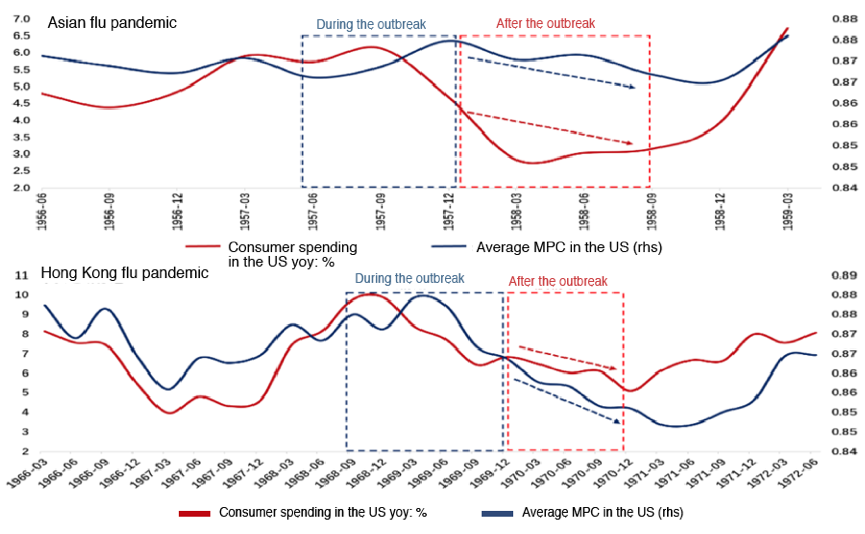

Theoretically, there are two factors that influence consumption: disposable income and marginal propensity to consume (MPC).

The restoration of MPC was very slow in the US after it went through major flu pandemics. Figure 8 shows that it took nearly a year for MPC in the US to recover after the outbreaks ended.

Assuming that the outbreak in China is mostly put under control in March or April, MPC is likely to restore by April next year. In this sense, the recovery of willingness to consume is not simple.

Figure 8: The recovery of willingness to consume will be slow after the pandemic

Source: Wind; author's calculation

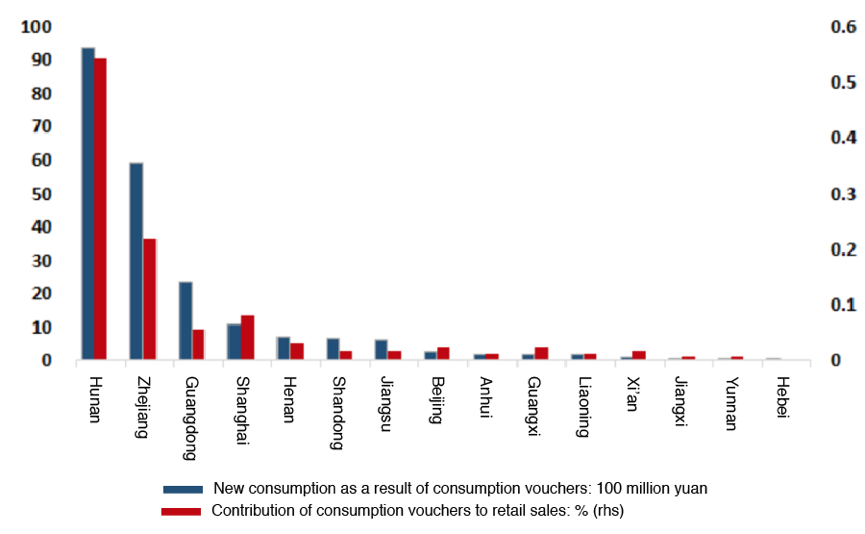

Second, the recovery of consumption is linked to disposable income. During economic downturns brought on by epidemics, unemployment would rise, wages and bonuses would fall sharply, and disposable income would also fall. The contribution of consumption vouchers at the current order of magnitude to consumption and investment in the whole economy is actually quite weak. It does have marginal effect, but the magnitude of its effect is worth further measuring.

Figure 9: The driving effect of consumption vouchers is likely limited

Source: Wind; author's calculation

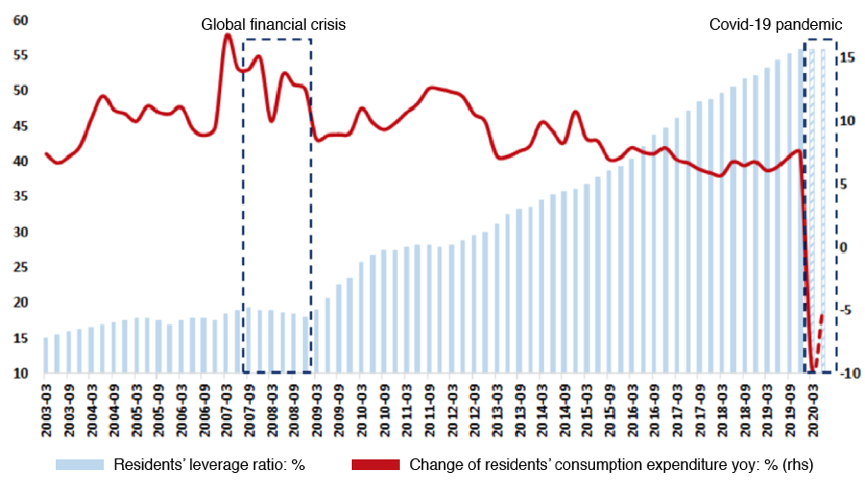

In addition, the more troublesome issue for consumption in China is that unlike the global financial crisis: while this time it is also facing external shocks, the household leverage is not what it used to be.

According to BIS, during the subprime crisis when China implemented the subsidy program for purchases of home appliances in countryside and auto stimulus, household debt ratio was only about 15%, but now it has reached 60%, so marginal effect of these policies can hardly drive consumption to the previous level.

Figure 10: Residents' debt burden has risen sharply, making consumption restoration even harder

Source: Wind; author's calculation

Countries' post-disaster or post-outbreak experiences show that the policy focus during the outbreak is on relief, but once the outbreak is under control, investment is also critical in addition to consumption.

Some people argue against investment as it can trigger problems such as redundant construction and high leverage. But the purpose of investment could be to strengthen the weak links, such as effective investments in the development of metropolitan areas and inter-city rail services. This is an urgent issue considering the current macro policy intensity.

IV. Economic recovery will be unbalanced

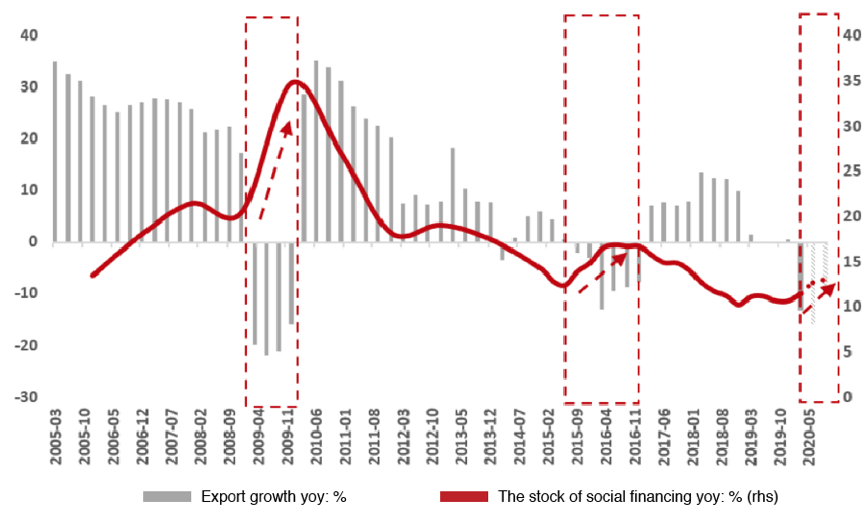

The speed of the current economic recovery largely depends on the strength of counter-cyclical policies. Historical data show that when external demand falls sharply, domestic monetary and fiscal policy space is usually opened to hedge against the severe challenges of economic downturn, and credit will expand significantly.

Especially in the second quarter, external demand may fall off a cliff, and corporate profits will fall sharply. In order to back government's debt issuance, the inter-bank market interest rate will likely be relaxed in a marginal sense in the future. In general, some trends are simply irresistible. Under the current context when external demand falls sharply, domestic monetary and fiscal policy space will be opened to hedge against the severe challenges of economic downturn, and credit will tend to expand.

Figure 11: Credit expansion will be the trend

Source: WIND

Since employment is a lagging indicator, the second and third quarters, instead of the first quarter, will experience the worst employment in China. The pressure to rescue the labor market and create more jobs in the second and third quarters will be enormous.

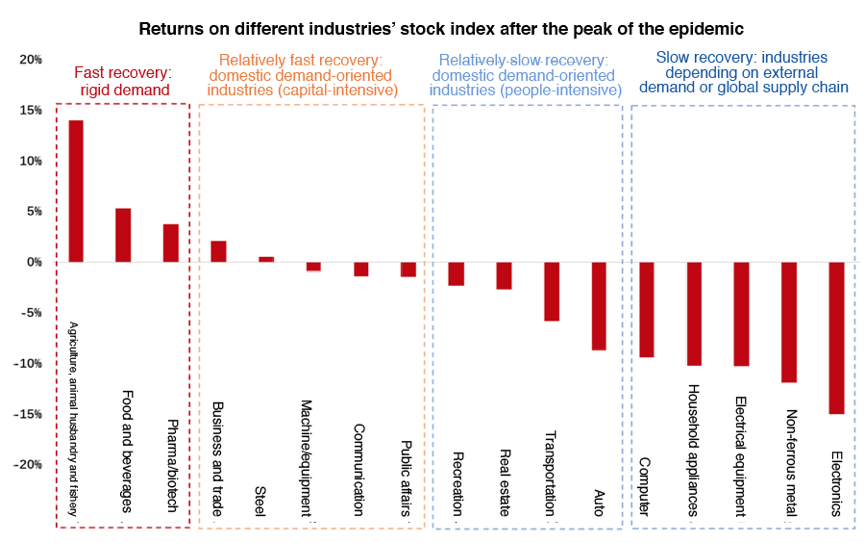

The Chinese economy is already on the way of recovering, but the characteristics of the epidemic shock implies that the recovery will be unbalanced: recovery of domestic demand will be faster than that of external demand; recovery of capital-intensive industries will be faster than that of people-intensive industries; and industries that rely on the global industrial chain and external demand may still be constrained in the future. It seems that such market expectations are reflected by the performance of various industries' stock indexes after the peak of the epidemic in China.

Figure 12: The speed of recovery varies among different economic sectors